A new era of taxation in Mexico for the digitalised economy[1]

(Article originally published for International Tax Review: https://www.internationaltaxreview.com/article/b1svjy367rx83n/a-new-era-of-taxation-in-mexico-for-the-digitalised-economy )

In October 2015, the OECD made public the action plan to combat tax evasion and profit shifting (BEPS). This plan consists of 15 measures that seek to redesign the international tax system by establishing mechanisms to combat aggressive tax practices and to ensure that taxpayers are taxed where they create value.

Action 1 of the plan (tax challenges arising from digitalisation) at the time of the issuance of the plan, remained unfinished. Initial differences of opinion as to the scope of the proposal, specifically whether it should be confined to digital companies or rather consider a ‘digitalisation of the economy’ approach, the design of mechanisms to attack the ‘lack of taxation’ of purely digital companies, the threat of the appearance of digital taxes and even the possibility of a trade war made negotiations difficult.

It was towards the beginning of President Biden’s administration in the US that the unified approach proposal (pillars one and two) preliminarily presented by the OECD’s Centre for Tax Policy and Administration, entered a new phase of negotiation that, in its last stage, finally led to a preliminary agreement and the issuance of a joint declaration by 132 of the 139 countries of the OECD’s inclusive framework on July 1 2021.

This proposal consists of the redistribution of taxation rights from the countries of residence of multinational companies to the countries from which they obtain their income, whether or not they have a physical presence in those countries (pillar one).

Additionally, it proposes the establishment of a global corporate tax rate of at least 15% (pillar two). It should be noted that the unified approach proposal is not specifically directed at digital companies or companies in the process of digitalisation, but seeks to tax the large multinationals (the OECD estimates that the 100 largest groups in the world would be subject to these new taxation rules).

The proposed unified approach in its pillar one reaches multinational groups with revenues of more than €20 billion (approximately $23 billion) and a profitability (profit before tax/revenue) of at least 10% (excluding companies in the financial and extractive sectors). Countries with taxing rights (nexus) on pillar one will be those in which multinational groups earn revenues of at least one $1 million, or even €250,000 in the case of countries with a gross domestic product of less than €40 billion.

Pillar two would have a much broader scope to include multinational groups with revenues of €750 million (the same threshold that was established for multinational groups that are required to file the BEPS Action 13 report), excluding only multinational groups in the international shipping sector.

Pillar two works through a set of global anti-base erosion (GloBE) rules which would work as follows according to the OECD’s statement on the two-pillar solution to address the fiscal challenges of the digitalisation of the economy of July 1 2021:

- An income inclusion rule (IIR), which would assign a supplementary tax to the parent company with respect to the under-taxed income of a group member entity; and

- An undertaxed payment rule (UTPR), which would deny deductions or require an equivalent adjustment to the extent the low tax income of a constituent entity is not subject to tax under an IIR; and

- Finally a regulation based on treaties (subject to the tax rule (STTR)) that allows source jurisdictions to impose limited taxation on certain taxable related party payments below a minimum rate. The STTR would be creditable as a covered tax under the GloBE rules.

The implementation of pillar one is expected to collect at least $100 billion, while from pillar two, $150 billion. If the negotiation comes to fruition this month of October (there are countries even within the EU that have abstained from signing the joint declaration of the OECD’s inclusive framework, such as Ireland, Estonia and Hungary), this long-awaited and much discussed reform of the international tax system is expected to be implemented in 2023.

Now, what would be the scope of the benefits that could be expected in Mexico? The following is an estimation of the impact that the implementation of this reform will have in Mexico.

Potential benefit for Mexico with the implementation of pillar one

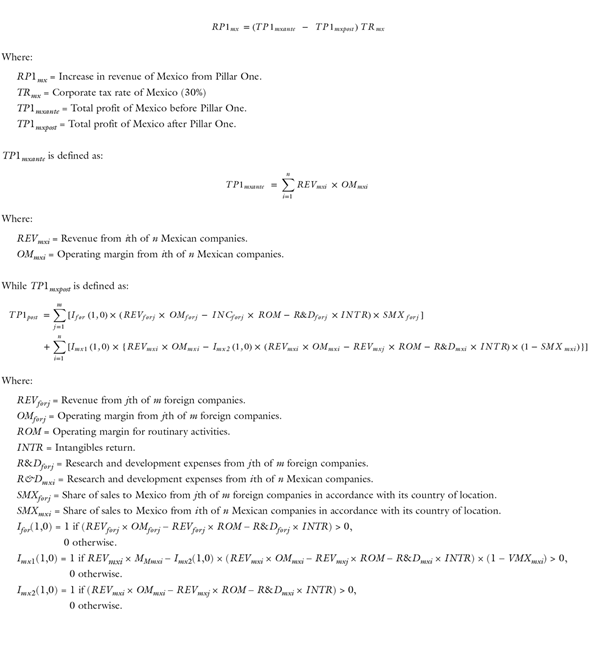

The benefit for Mexico of the implementation of pillar one would be given by the differential of the outflow of resources attributable to Mexican companies v. the income of resources from foreign companies that are within the scope of the proposed regulation.

To identify eligible multinational groups, a search was conducted in the Bureau Van Dijk Osiris database in order to identify multinational groups that reported revenues in excess of €20,000 million and an operating margin greater than 10%, excluding mining and financial sector companies. The analysis was focused on fiscal year 2019 to avoid distortions generated by the COVID-19 pandemic.

Of the sample obtained, only one Mexican company (América Móvil) exceeded the thresholds established by the OECD for pillar one. On the other hand, 146 foreign multinational groups were considered for the analysis. Each of these groups was assigned a percentage of sales to Mexico based on the country in which it is located (this data is obtained from the OECD’s AMNE 2016 database). In the case of countries for which there is no information in the database, the percentage of sales to Mexico of the world total is assigned.

From each group three types of variables are used: revenue, operating margin and research and development expenses (from 2019).

The calculation of the increase in revenues is expressed in Equation 1.

Equation 1

(Click to enlarge)

Potential benefit for Mexico with the implementation of pillar two

For the calculation of the pillar two benefit, a search was conducted in the Bureau Van Dijk’s Osiris database for foreign companies reporting revenues in excess of €750 million in 2019.

Maritime companies and Mexican multinationals were excluded from the sample since a minimum corporate tax rate is not considered above the rate in Mexico. Each company is assigned the corporate tax rate of the country where it is located (data obtained from taxfoundation.org).

The equation that then expresses the income for Mexico by implementing pillar two is shown in Equation 2.

Equation 2

(Click to enlarge)

In consideration of the status of the negotiation of pillar two, in relation to the parameters of return on routine activities, return on generation of intangibles and the minimum rate, the results are evaluated for different scenarios in the increase in revenue for Mexico in both pillar one and pillar two.

Estimated revenue increase for Mexico under pillar one

| $K | Intangibles | |||

| 0% | 15% | 25% | ||

| Routinaries | 5% | $1,096,631 | $1,035,346 | $994,490 |

| 7.5% | $940,286 | $879,001 | $838,185 | |

| 10% | $783,941 | $723,496 | $683,829 |

Estimated revenue increase for Mexico under Pillar Two

| Minimal $K | ||

| 15% | 17.5% | 20% |

| $501,734 | $613,289 | $787,908 |

The results indicate that the combined benefit of the impact of both pillars for Mexico in the intermediate scenario would be $1,553 million and could reach up to $1,884 million in the best of the scenarios evaluated in this article.

It should also be noted that to the extent that a lower remuneration is agreed for routine activities, that intangibles are not remunerated or are remunerated in the lowest possible amount and that the minimum rate is agreed at a higher level; higher revenues can be expected for Mexico.

Final considerations

The implementation of the unified approach proposal generates a net benefit for Mexico in view of the low number of Mexican multinationals that exceed the limits established in pillar one.

The maximum expected benefit of up to $1,884 million (more than 37 billion pesos) could easily cover three times the entire budget of the National Council of Science and Technology (322%), almost two times the budget of the National Electoral Institute (189%), or the Environment and Natural Resources (up to 119% of its budget, according to figures from the Federal Expenditure Budget, 2020).

Evidently, the inflow of resources to Mexico would have to be compared against what would have been possible to capture via a local digital tax, or through proposals such as the one presented by the UN in Article 12-B of its Model Tax Convention which was built in parallel to the OECD’s unified approach proposal.

In any case, the approval of pillars one and two seems imminent, and with it, the establishment of a formulary approach to complement the arm’s-length system in response to the challenges of the digitalised economy, thereby inaugurating a new era in international taxation.

[1] Jesús Aldrin Rojas & José Chamorro Gómez